What is product liability insurance, and who needs it?

Product liability insurance protects businesses from legal and financial claims when a product causes bodily injury, property damage, or harm to a third party. If you make, sell, distribute, or supply physical goods, this coverage belongs in your policy stack. Full stop.

Who needs it most? These business types carry the highest exposure:

- Manufacturers and contract manufacturers producing chemical, industrial, or consumer goods

- Wholesalers and distributors moving products through the supply chain

- Retailers selling goods they did not make, since strict liability laws can hold every party in the chain responsible

- Private label brands whose name appears on a product regardless of who formulated it

- Importers bringing foreign-made goods into the U.S. market

One common misconception: many manufacturers believe strict liability claims are uninsurable. They are not. Product liability coverage includes legal defense for strict liability claims, which means a customer only needs to prove the product harmed them, not that you were negligent. That distinction has real financial weight.

What does product liability coverage include, and what does it exclude?

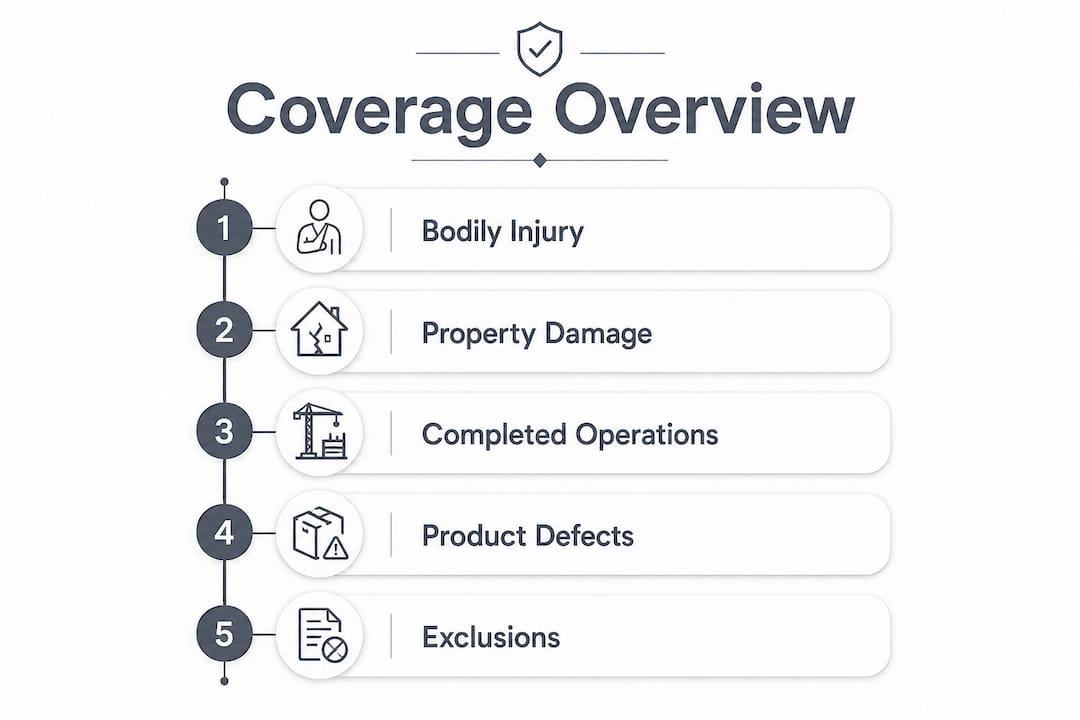

Coverage centers on three categories of product defects: design flaws, manufacturing errors, and marketing failures such as missing warnings or inadequate instructions. A solid policy pays for medical bills, legal defense costs, and settlements tied to any of these.

What a standard policy covers:

- Bodily injury caused by a defective product

- Property damage resulting from product failure

- Legal defense costs, even for meritless claims (without defense coverage, legal fees alone can reach six figures)

- Claims arising from completed operations, meaning products already delivered and in use

What it typically excludes:

- Product recall costs, which require a separate recall policy

- Intentional misconduct or fraud

- Damage to the product itself (a defective tire that destroys itself is not covered, but injuries caused by that tire are)

- Prior known defects the business failed to disclose

- Transportation of goods in transit and on-site inventory damage

Completed operations coverage is the most commonly overlooked gap. It protects your business after a product leaves your facility, filling the space between general liability and product liability. Check your policy for it before you sign.

How much does product liability insurance cost?

Premiums vary based on risk and business size, typically with a standard coverage minimum around the million-dollar level, though some product categories require higher limits.

Several variables drive your actual rate:

- Annual revenue and sales volume: higher revenue means more exposure and higher premiums

- Product type and risk profile: chemical manufacturers pay more than retailers of low-risk goods due to inherent hazards

- Safety documentation: detailed R&D logs, quality control records, and safety protocols lower your premium by demonstrating risk management to underwriters

- Business scale: a policy sized for pilot batch production will be inadequate once you reach full truckload output

Statistic callout: Premiums for lower-risk retail businesses can start at low monthly rates, while chemical and industrial manufacturers typically pay materially more, reflecting the higher frequency and severity of claims in those sectors.

Reviewing your policy as your business scales is not optional. A coverage limit that made sense at launch can leave you dangerously exposed after you enter a new product category or ramp production volume.

Comparing top U.S. product liability insurance providers for small businesses

Nine providers stand out for small businesses and manufacturers evaluating coverage options in 2026. Each serves a distinct segment, and the right fit depends on your industry, risk profile, and how you prefer to buy.

| Provider | Services offered | Specializations | Certifications and recognition | Positioning | Rating |

|---|---|---|---|---|---|

| Thimble | General liability, professional liability, BOP, workers' comp | Small businesses, contractors | A-Rated Insurance, Accredited Business | Pay-by-job, month, or year flexibility | 4.5★ (458) |

| The Hartford | Business, auto, home, employee benefits | Small business, AARP members | Endorsed by AARP, 200+ years in service | Trust-first insurer for people and businesses | 3.6★ (327) |

| Insureon | Small business insurance from top carriers | Micro and small businesses | #1 digital agency for small business insurance | Fast digital quotes from multiple carriers | 3.5★ (104) |

| Insurance Plus | Commercial, contractor, auto, renters, homeowners | Texas business and commercial insurance | Licensed Independent Insurance Agency | Texas-based agency with instant online quotes | 3.3★ (12) |

| US Insurance Company of America | Liquor liability, BOP, bonds, property and liability | Bars, restaurants, hospitality, retail | Specialist in liquor liability | Hospitality and retail liability specialist | 4.2★ (10) |

| United States Liability Insurance | General liability coverage | Broad U.S. client base | Licensed agency | Wide-reach liability coverage provider | 4.3★ (3) |

| Liability Insurance Solutions | Custom liability packages for various sectors | Diverse business needs | — | Tailored liability for multiple industries | 4.5★ (2) |

| USA PRO Insurance Group LLC | Auto liability, general liability, cargo, workers' comp | Fleets, logistics, contractors, owner-operators | — | Custom policies for high-risk transportation and contracting | 5★ (1) |

| truck insurance | Commercial vehicle and truck insurance | Logistics and transportation | — | Focused truck and vehicle liability expertise | 5★ (1) |

Thimble is built for speed. Its pay-per-job model suits contractors and small manufacturers who need coverage for a specific production run without committing to an annual policy. The A-Rated and Accredited Business credentials give it credibility beyond its flexible structure.

The Hartford carries the weight of over 200 years in business and an AARP endorsement, which signals stability for small business owners who want a carrier with a long track record. Its range covers business insurance, employee benefits, and more under one roof.

Insureon functions as a marketplace rather than a direct carrier. If you want to compare quotes from multiple top carriers without calling five different agents, Insureon's digital platform delivers that in minutes.

Insurance Plus suits Texas-based businesses specifically. As a licensed independent agency, it offers both instant online quotes and agent-assisted coverage for commercial and contractor liability.

US Insurance Company of America is the clearest specialist on this list for hospitality. Bars, restaurants, caterers, and liquor retailers will find its liquor liability depth hard to match elsewhere.

USA PRO Insurance Group LLC targets transportation and contracting businesses with custom policies covering fleets, owner-operators, and logistics companies, including cargo and off-route liability.

truck insurance focuses exclusively on commercial vehicles and trucking liability, a narrow specialty that matters when your exposure is on the road.

United States Liability Insurance and Liability Insurance Solutions both serve general liability needs across a broad client base, with limited public detail on specific specializations.

How to select the right product liability policy for your business

The right policy is not the cheapest one. It is the one that actually covers your specific risk.

Key factors to evaluate:

- Coverage limits: a $1 million minimum is standard; high-risk products or large distribution volume may require $5 million or more

- Exclusions: read them carefully, especially for completed operations, recall costs, and known defects

- Financial strength of the carrier: an A-rated insurer is less likely to dispute or delay a valid claim

- Claims handling reputation: ask how the carrier handles defense costs and whether defense is inside or outside the policy limit

- Bundling options: product liability is often included in a commercial general liability (CGL) policy, but not always

Questions to ask any provider before you buy:

- Does this policy include completed operations coverage?

- Are defense costs inside or outside the policy limit?

- What documentation do you need from me at underwriting?

- Does the policy cover strict liability claims?

- Can I add a Vendors Coverage endorsement if my retail partners require it?

Red flags to watch for:

- No completed operations coverage in the policy language

- Defense costs counted inside the liability limit (this reduces your actual payout capacity)

- Vague exclusion language around "known defects" without a clear definition

- No option to add Additional Insured endorsements for distributors or retailers

Pro Tip: Retailers and distributors often require proof of Vendors Coverage before they will carry your product. Verify that your policy includes this endorsement, or that you can add it, before you sign a distribution agreement.

Product liability risks specific to contract chemical manufacturing

Contract chemical manufacturers face a category of exposure that standard general liability policies are not built to handle. The risk profile is simply too concentrated.

General liability covers premises accidents and broad business operations. It does not go deep enough for chemical manufacturing claims, where strict liability applies and a single batch error can trigger claims across an entire distribution chain. A monoline product liability policy, purchased separately, is often the right structure for this sector.

Key considerations for contract manufacturers:

- Vendors Coverage endorsement: required by most retailers and distributors before they will list your product

- Additional Insured status: your retail and wholesale partners will ask to be named; build this into your policy from day one

- Discontinued product coverage: if you stop making a formula, claims can still arrive years later; confirm your policy covers discontinued lines or purchase tail coverage

- Recall coverage: this is always a separate policy. Standard product liability does not cover the cost of pulling a product from shelves, managing public communications, or repairing a defect at scale

- Safety documentation: underwriters evaluate your R&D logs, batch records, and quality control protocols directly. Thorough documentation lowers your premium and improves your insurability

The more transparent your safety process, the better your underwriting outcome.

How to evaluate and choose a product liability insurance provider

Choosing a provider comes down to three things: financial strength, fit for your industry, and how they handle claims.

Start with the carrier's financial rating. An A-rated insurer, as recognized by AM Best, has the reserves to pay large claims without dispute. Next, confirm the provider has genuine experience in your product category. A hospitality specialist like US Insurance Company of America brings depth that a generalist carrier cannot match for a bar owner. A transportation-focused provider like USA PRO Insurance Group LLC understands fleet exposure in ways a small business generalist does not.

Finally, ask about claims handling before you buy. How quickly does the carrier assign a defense attorney? Are defense costs inside or outside your limit? A policy with defense costs inside the limit effectively reduces your coverage the moment a claim is filed.

Sarawestusa builds the products that need this coverage

The providers compared above protect businesses after something goes wrong. Sarawestusa is where the product gets built right from the start.

We manufacture contract chemical formulations across eight industries, from commercial cleaning to sports care, using in-house R&D chemists who document every formula, every batch, and every safety protocol. That documentation is exactly what insurers want to see when they underwrite a chemical manufacturing policy. Transparent process, real accountability, and a library of over 1,200 proven formulas mean your product arrives with a paper trail that supports your coverage, not one that complicates it. If you are sourcing products for wholesale or private label and need a manufacturing partner whose process holds up to underwriter scrutiny, we are ready. Tell us what you need made.

Key Takeaways

Product liability insurance is the financial foundation every product-based business needs before a single unit ships.

| Point | Details |

|---|---|

| Coverage scope | Policies cover bodily injury, property damage, design defects, manufacturing errors, and inadequate warnings. |

| Recall costs are excluded | Product recall coverage requires a separate policy; standard product liability does not include it. |

| Cost drivers | Premiums for low-risk retail businesses can be highly affordable, while chemical manufacturers generally pay higher rates due to their risk profile and safety documentation requirements. |

| Policy gaps to close | Completed operations coverage and Vendors Coverage endorsements are commonly missing and commonly required by retail partners. |

| Sarawestusa's role | Sarawestusa's documented R&D and batch records support stronger underwriting outcomes for contract chemical manufacturing clients. |